Refinance Break-Even Point: The Two Numbers That Decide If Refinancing Is Worth It

Your refinance break-even point is the month your accumulated savings finally cancel out the closing costs. Most lenders quote it as one tidy number: $7,000 in costs ÷ $280 a month saved = 25 months. Clean, and slightly wrong. There's a second break-even hiding underneath that one — usually 6 to 12 months later — and it's the number that actually tells you whether refinancing builds wealth. Miss it and you can "break even" on paper while quietly falling behind.

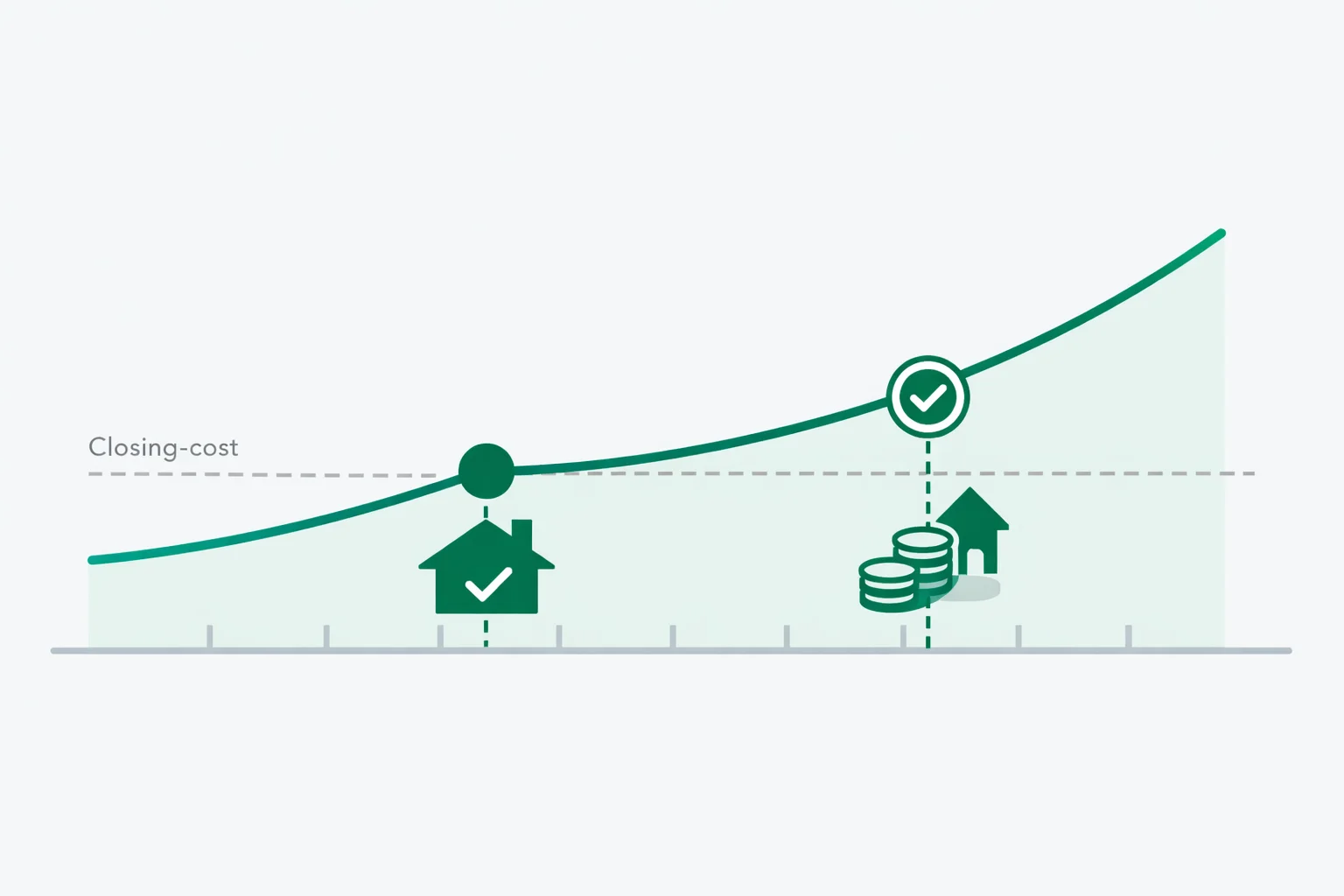

Your Lender Quotes One Break-Even — There Are Two

The break-even your loan officer shows you is the simpleone: how long until the payment savings add up to the closing costs. It's easy to calculate and easy to understand, which is exactly why it's the only one anyone mentions. The problem is it ignores equity.

When you refinance — especially into a fresh 30-year term — you start paying down principal more slowly than your old loan did. That slower equity build is a real cost. The true break-evencounts it: it's the month your total net worth (cash saved plusequity built, minus closing costs) turns positive. Because you're giving up some equity speed, the true number always lands at or after the simple one. On a term reset it can be a full year later. The full mortgage refinance calculator and this break-even tool answer different questions — one shows lifetime savings, this one shows the recovery deadline.

The Simple Break-Even Formula

Start with the version everyone uses, because it's still the right first filter:

Break-even months = total closing costs ÷ monthly payment savings

Say your closing costs are $6,500 and your payment drops by $260 a month. That's $6,500 ÷ $260 = 25 months. Twenty-five payments in, you've recovered what you spent; every payment after that is genuine savings. The monthly-savings half of that fraction comes straight from the rate cut — you can see exactly how a rate change shifts your principal-and-interest split with our principal and interest calculator. Two things move this number, and both matter more than the rate itself: how big the closing costs are, and how much the payment actually falls.

Why the True Break-Even Lands Later

Here's the part the simple formula misses. Imagine you're 4 years into a 30-year loan with 26 years left. You refinance into a new 30-year. Your rate dropped, so the payment fell — good. But your loan clock just reset to year zero, where almost every dollar goes to interest instead of principal.

In the first year after that reset, you might build $1,200 less equity than you would have on the old loan, even though your payment is lower. That lost equity is a cost the cash-only break-even never sees. The true break-even adds it back: it waits until your cash savings have covered both the closing costs and the equity you gave up. Keep the same term you had left — refinance 26 years into a new 25- or 26-year loan — and the gap between the two break-evens nearly disappears. Watch the equity curve reset for yourself with the mortgage amortization calculator; it's the clearest picture of why term choice drives the true number.

Worked Example: Recovering $7,000 in Costs

Let's run a real one. You owe $280,000 at 7.0% with 26 years left, paying $1,944 a month. You're quoted 5.75% on a new 30-year with $7,000 in closing costs. The new payment is $1,634. Step by step:

- Monthly savings: $1,944 − $1,634 = $310

- Simple break-even: $7,000 ÷ $310 ≈ 23 months

- Equity given up: in the first two years the reset 30-year builds roughly $1,100 less principal than the old loan would have

- True break-even: about 31 months — eight months past the simple number, once that lost equity is counted

If you're staying 10 years, this is an easy yes: you clear both break-evens with years to spare and net tens of thousands. But if you might sell in 28 months, the simple number says "you're fine" while the true number says "you barely recovered, and your equity is behind." That eight-month spread is the difference between a smart move and a wash. Price the new payment first with a plain mortgage calculator so your savings figure is solid before you trust either break-even.

How Closing Costs Move Your Break-Even

People obsess over the rate and shrug at closing costs. That's backwards — closing costs are the entire numerator of the break-even fraction. Here's how the recovery period stretches as costs climb, holding the savings steady at $310 a month from the example above:

| Closing Costs | Simple Break-Even | ~True Break-Even | Net at 5 Years |

|---|---|---|---|

| $3,500 | 12 months | ~19 months | +$15,100 |

| $5,500 | 18 months | ~26 months | +$13,100 |

| $7,000 | 23 months | ~31 months | +$11,600 |

| $9,500 | 31 months | ~40 months | +$9,100 |

Every extra $1,000 in costs pushes the simple break-even out by roughly three months at this savings level. That's why shaving fees matters: negotiate the lender origination charge, shop title insurance separately, and check whether your existing servicer waives the appraisal. Use our closing costs calculator to itemize the bill before you accept a quote — a $2,000 reduction can pull your break-even forward by half a year. Per the CFPB's Loan Estimate guidance, every lender must hand you a standardized cost breakdown within three business days of applying — the page-2 totals are what you plug in here.

The Timeline Test: Break-Even vs. How Long You Stay

A break-even number means nothing on its own. It only matters next to one other date: when you'll sell the house or refinance again. That's the deadline your break-even has to beat. Decide like this:

- Staying well past the true break-even (5+ years of cushion)? Refinance — you capture years of clean savings and the equity gap closes on its own.

- Staying just past the simple but short of the true break-even? Borderline. You'll recover cash but your equity lags. Worth it only if cash flow is the priority, not net worth.

- Leaving before the simple break-even?Don't refinance the normal way. Look at a no-closing-cost version instead, which skips the upfront hit entirely.

The median American homeowner sells or refinances within roughly 8 to 10 years, so a 24- to 36-month break-even is usually safe. But "usually" isn't your situation. A job relocation, a growing family, or a planned downsize can move your real horizon to three years — and a 31-month true break-even you felt great about suddenly has almost no margin.

Do Points Help or Hurt Your Break-Even?

Discount points are a side bet on how long you'll stay. Each point costs 1% of the loan and typically buys the rate down about 0.25%. On a $280,000 refinance, one point is $2,800 and might lower the payment around $45 a month. That's a 62-month break-even on the points alone — over five years just to recover the points, on top of recovering your base closing costs.

The logic is simple once you frame it as its own break-even. Buying points only wins if you'll keep the loan far longer than the point's payback period. Planning to stay 12 years? Points can save real money. Thinking 4 years? Skip them, take the slightly higher rate, and keep the $2,800 working as a smaller break-even instead. Never let a lender bundle points into the quote without breaking out their separate payback — it's a common way to make a rate look better than the deal really is.

Break-Even Mistakes That Cost Real Money

- Trusting the simple break-even on a term reset. Refinancing 22 years left into a new 30-year and reading only the cash break-even can hide a year of lost equity. Match the term to your remaining years and the two break-evens line up.

- Ignoring rolled costs.Financing $7,000 of fees into the balance feels free, but you pay interest on them for decades and your net-worth break-even still exists — it's just buried. The cash-out math works the same way; if you're also pulling equity, run a cash-out refinance calculator because adding cash re-rates the whole loan.

- Counting prepaid escrow as a true cost.Some of your "closing costs" are prepaid taxes and insurance you'd owe anyway, plus an old escrow balance that gets refunded. Strip those out before computing break-even or you'll overstate your recovery period by a month or two.

- Chasing a break-even shorter than your loan needs to be. A 16-month break-even is meaningless if you sell at month 14. The horizon always wins the argument — measure it honestly.

One last habit that pays off: pull written Loan Estimates from at least three lenders on the same day. The Freddie Mac rate survey shows the spread between lenders on identical loans routinely runs a quarter point or more — and a lower rate or smaller fee on even one quote can pull your true break-even forward by half a year.