Interest-Only Mortgage Calculator: Short-Term Savings vs Long-Term Costs

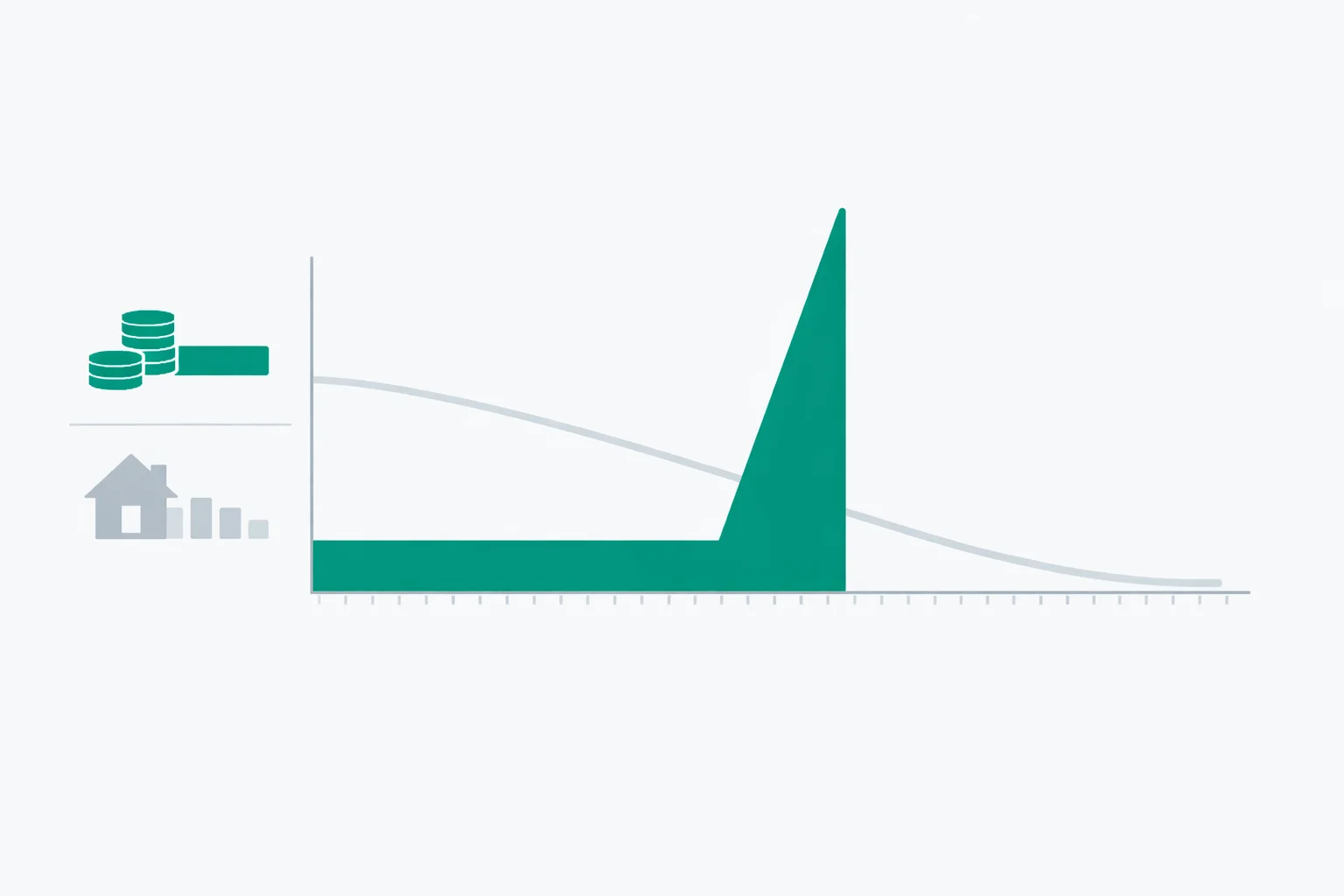

An interest-only mortgage calculator answers one question most borrowers never think to ask until year 11: what does my payment look like the day the training wheels come off? During the IO period you pay only the interest charge — on a $400,000 loan at 7%, that's $2,333 a month, flat. Then the principal repayment window opens, your payment jumps to $3,101, and nothing in your budget changed to prepare for it.

The math itself is unusually clean. What makes these loans tricky is not the formula — it's the behavior the structure encourages. Borrowers treat the low early payment as the real cost of the loan and the shock as a future problem. This guide walks through the numbers at every stage so there are no surprises.

Why the IO Payment Formula Is So Simple

A standard amortizing mortgage needs the full amortization formula with an exponent, a numerator, a denominator, and usually a calculator. An interest-only payment is one multiplication. The formula is:

Monthly IO payment = Loan amount × (Annual rate ÷ 12)

At 7.0% on a $400,000 loan, that's $400,000 × (0.07 ÷ 12) = $400,000 × 0.005833 = $2,333.33. Every dollar of that payment goes to interest. Your balance at month 120 is the same $400,000 you borrowed on day one. No equity from payments, no reduction in what you owe the bank — just rent on the money.

When the IO period ends, the lender recalculates what payment fully retires your balance over the remaining term. On the same loan with a 10-year IO period and a 30-year total term, you now need to amortize $400,000 over 20 years at 7%. That works out to $3,101 per month. The bank doesn't ask whether your paycheck kept up.

A $400,000 IO Loan — From Month 1 to Year 30

Let's run a complete scenario. You borrow $400,000 at 7.0% with a 10-year interest-only period and a 30-year total term. Here's what actually happens month by month:

- Years 1-10: You pay $2,333.33 per month, 120 months in a row. Total paid: $280,000. Total interest: $280,000. Principal paid: $0. Balance at month 120: $400,000.

- Year 11, month 1: Payment recalculates. The remaining $400,000 must amortize over 20 years at 7%. New payment: $3,101.31.

- Years 11-30: 240 payments at $3,101.31. Total paid in this phase: $744,314. Of that, $344,314 is interest and $400,000 retires the principal.

- Lifetime totals: You paid $1,024,314 over 30 years. $624,314 was interest. The home cost you $400,000 plus $624,314 in interest.

For comparison, the same $400,000 financed as a standard 30-year mortgage at the same rate would cost $2,661 per month and $557,843 in total interest. The IO structure cost you roughly $66,000 extra in interest over the life of the loan — but it also meant paying $328 less per month during the first decade, which is $39,360 of cash flow you kept.

Payment Shock by IO Period Length

The length of the IO period is the single biggest driver of shock severity. Shorter IO periods produce smaller shocks because the amortization window is longer. The table below assumes a $400,000 loan at 7% with a 30-year total term.

| IO period | Amortization window | IO payment | Amortizing payment | Payment shock |

|---|---|---|---|---|

| 3 years | 27 years | $2,333 | $2,744 | +$411 (+18%) |

| 5 years | 25 years | $2,333 | $2,827 | +$494 (+21%) |

| 7 years | 23 years | $2,333 | $2,934 | +$601 (+26%) |

| 10 years | 20 years | $2,333 | $3,101 | +$768 (+33%) |

| 15 years | 15 years | $2,333 | $3,595 | +$1,262 (+54%) |

A 15-year IO period sounds attractive on the front end — more time with lower payments — but it compresses the entire principal repayment into the back half of a 30-year term. The shock is brutal: a 54% payment jump on a budget that just got used to a much lower number.

How Much the IO Rate Premium Actually Costs

Interest-only mortgages almost always carry a rate premium over conventional loans because they represent more risk to the lender. Freddie Mac doesn't buy most IO mortgages, so they sit on bank balance sheets or get sold into private-label securities. That premium typically runs 0.25% to 0.75% above the prevailing 30-year rate. According to the CFPB, this premium combined with the non-amortizing structure can substantially increase the total cost of borrowing.

On our $400,000 example, a 0.50% rate premium (7.5% vs 7.0%) adds up fast. At 7.5%, the IO payment rises to $2,500/month — $167 more than the 7.0% version. Over 10 IO years, that's $20,000 in extra interest before principal repayment even starts. Plug both rates into the mortgage calculator and compare the 30-year totals side-by-side before accepting an IO quote.

Who Interest-Only Loans Actually Work For

IO mortgages aren't universally bad — they're just badly matched to the average buyer. They genuinely work for four specific borrower profiles:

- Bonus-heavy earners. Wall Street, tech, commission sales — anyone whose base pay covers the IO payment and whose annual bonus lump-sums principal down. The low fixed payment keeps cash flow predictable when the bonus arrives late.

- Short-term owners. If you know with high confidence you'll sell within the IO window (relocations, medical residents, military), the amortization shock never hits you. You capture the lower payment and exit before the reset.

- Investors with cash-flowing rentals. Lower mortgage payments mean more free cash flow per unit, and the investor can direct that cash into property improvements or additional acquisitions. The tax treatment of interest also plays cleaner when payments are 100% deductible interest.

- High-net-worth borrowers with illiquid assets. A business owner whose wealth is locked in equity can use an IO mortgage to avoid selling assets while still buying a home. The plan is usually to pay off the balance from a planned liquidity event.

The Zero-Equity Trap Most Borrowers Don't See

Here's the mental model shift: during the IO period, your mortgage payment doesn't build wealth — it buys you time. Compare two buyers who both put $100,000 down on a $500,000 home:

- Buyer A (standard 30-year mortgage): After 10 years at 7%, they've paid down $64,000 of principal. Combined with the $100,000 down payment, they have $164,000 in equity from payments alone, plus any appreciation.

- Buyer B (10-year IO, 30-year total): After 10 years, they've paid down $0. Their equity is still just the $100,000 down payment, plus whatever the home appreciated.

If home values drop 10% during those 10 years — which has happened in multiple regional markets — Buyer B's $100,000 down payment gets cut to $50,000 of remaining equity against a $400,000 loan. Buyer A still has $114,000. To see exactly how that paydown builds on a standard amortizing loan, run the principal and interest calculator, or check what you'll actually own with the home equity calculator before assuming appreciation will rescue the strategy.

Using Extra Principal to Defuse the Shock

Every IO mortgage this author has ever reviewed allows voluntary principal payments without penalty. That option is the single most useful hedge against payment shock. The mechanism is worth understanding because the effect compounds:

- Extra principal reduces the balance, which reduces the interest charge next month.

- Lower interest charge means a bigger share of your next extra payment also hits principal.

- When the IO period ends, the balance being amortized is smaller, so the new payment is smaller too.

Concrete example: on the $400,000 / 7% / 10-year IO baseline, paying an extra $500/month during the IO period reduces the balance at month 120 from $400,000 to roughly $313,500. The amortizing payment over 20 years at 7% drops from $3,101 to about $2,431 — a shock of just $98/month instead of $768. That cut in future monthly pain cost you $60,000 in extra cash over the IO period, but it protected $670/month of future budget for 240 months.

IO Mortgage vs HELOC vs 10/1 ARM

These three products get confused constantly. They solve different problems:

| Product | Position | Rate type | Principal? | Best for |

|---|---|---|---|---|

| Interest-only mortgage | First | Fixed (usually) | Deferred | Buying the home, predictable payments |

| HELOC | Second | Variable | Deferred during draw | Flexible access to equity |

| 10/1 ARM | First | Fixed 10 yrs, then variable | From day 1 | Rate-betting on declining rates |

The 10/1 ARM is the most commonly confused alternative. It also has a 10-year honeymoon phase, but during that time you're making full principal-and-interest payments — the "10" refers to when the rate can start adjusting, not when principal payments start. If your goal is low initial payments, the IO mortgage is more aggressive; if your goal is rate protection with normal amortization, the ARM is cleaner.

When an Interest-Only Mortgage Is the Wrong Choice

There are three situations where an IO mortgage looks attractive but quietly destroys wealth:

- Using it to stretch into a more expensive home. If the standard 30-year payment is unaffordable and the IO payment is what makes the purchase "work," you are buying a house you cannot afford. The amortizing payment arrives eventually, and when it does, nothing has improved — except now you have 10 years of zero-equity ownership behind you.

- Counting on appreciation to bail you out. A FHFA House Price Index review shows that regional housing markets can move sideways or decline for 5+ year stretches. An IO mortgage in a flat market leaves you with the original debt and no paydown to show for the decade.

- Without a written exit plan. Every good use of an IO loan has a specific plan: sell in year 7, refinance when rates drop, pay off with the business sale. "I'll figure it out later" is not a plan — it's how people end up forced to sell the week the amortization starts.

The pro move: before signing an IO loan, write down the date the amortizing payment begins and the exact dollar amount. Stick that on the fridge. Check your affordability ratioagainst the post-IO payment, not the IO payment. If the amortizing number doesn't fit, the loan doesn't fit — the IO phase is just delaying the math.