Simple Interest Explained: How the I=PRT Formula Works with Real-World Examples

A simple interest calculator lets you find out exactly how much interest you'll earn — or owe — on any principal amount using the straightforward I = P × R × T formula. Unlike compound interest, which snowballs over time, simple interest is calculated only on the original principal. That makes it the standard method for auto loans, short-term personal loans, promissory notes, and Treasury bills. Whether you're evaluating a 36-month car loan at 6.5% or figuring out how much a $15,000 promissory note returns in 2 years, this guide walks you through the formula step by step with real dollar amounts.

What Is Simple Interest?

Simple interest is a method of calculating the cost of borrowing money — or the return on an investment — based solely on the original principal. The interest amount stays the same each period because it never compounds. If you deposit $10,000 at 5% simple interest, you earn exactly $500 every year: $500 in year one, $500 in year two, and so on. The bank doesn't add last year's interest to your principal before calculating next year's return.

This predictability is both the advantage and the limitation of simple interest. Borrowers benefit because total interest costs are lower and fully predictable from day one. Savers and investors, on the other hand, miss out on the exponential growth that compound interest provides over long time horizons.

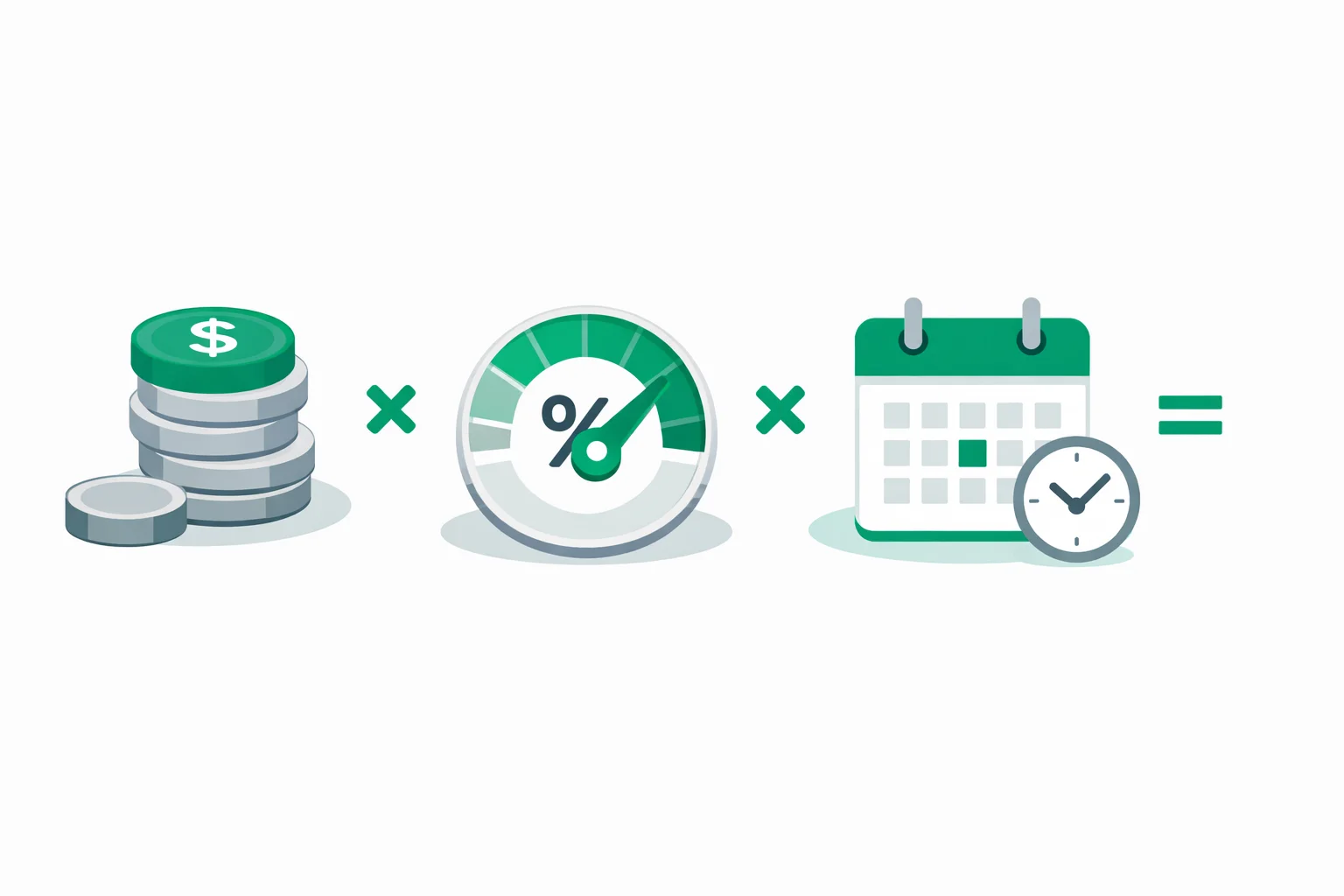

The Simple Interest Formula (I = P × R × T)

The formula has three variables:

- P (Principal)— the original amount of money. For a loan, this is how much you borrow. For an investment, it's your starting deposit.

- R (Rate) — the annual interest rate expressed as a decimal. Convert a percentage by dividing by 100: 6% becomes 0.06.

- T (Time)— the duration in years. For months, divide by 12. For days, divide by 365 (or 360 using the banker's convention).

The total amount you'll have (or owe) at the end is: A = P + I, where A is the final amount and I is the interest calculated by the formula.

Worked Examples with Real Dollar Amounts

Example 1: Auto loan.You borrow $25,000 at 6% simple interest for 5 years. I = 25,000 × 0.06 × 5 = $7,500. You'll pay back a total of $32,500. That's $125 per month in interest alone ($7,500 ÷ 60 months).

Example 2: Short-term business loan.A small business borrows $50,000 at 8% for 18 months. First convert months to years: 18 ÷ 12 = 1.5 years. I = 50,000 × 0.08 × 1.5 = $6,000. Total repayment: $56,000.

Example 3: 90-day Treasury bill.You invest $10,000 in a T-bill yielding 5.25%. Time in years: 90 ÷ 365 = 0.2466. I = 10,000 × 0.0525 × 0.2466 = $129.44. After 90 days, you'll have $10,129.44.

Example 4: Finding the required principal.You need to earn $3,000 in interest over 2 years at 4%. Rearrange the formula: P = I ÷ (R × T) = 3,000 ÷ (0.04 × 2) = $37,500. You'd need to invest $37,500 to hit your target.

Simple Interest vs. Compound Interest

The difference between simple and compound interest grows dramatically over time. Here's a side-by-side comparison on a $10,000 principal at 6%:

| Time Period | Simple Interest | Compound (Monthly) | Difference |

|---|---|---|---|

| 1 year | $600 | $617 | $17 |

| 5 years | $3,000 | $3,489 | $489 |

| 10 years | $6,000 | $8,167 | $2,167 |

| 20 years | $12,000 | $23,102 | $11,102 |

| 30 years | $18,000 | $50,226 | $32,226 |

At 1 year the gap is just $17 — barely noticeable. But by 30 years, compound interest earns nearly three times more. This is why simple interest is common for short-term loans (where the gap is small) while savings accounts and investments almost always use compounding. Use our compound interest calculator to see how your money grows with compounding at different frequencies.

Key Factors That Affect Simple Interest

- Principal size: Doubling your principal doubles your interest. A $20,000 loan at 5% for 3 years costs $3,000 in interest versus $1,500 on a $10,000 loan — exactly proportional.

- Interest rate: A 1% rate increase on $25,000 over 5 years adds $1,250 in total interest. Small rate differences matter most on larger loans with longer terms.

- Time period:Each additional year adds one full year's worth of interest. On $10,000 at 6%, that's an extra $600 per year — no more, no less.

- Day-count convention:Some lenders use a 360-day year (banker's method) instead of 365. On a $50,000 loan at 7% for 180 days, the 360-day method charges $1,750 versus $1,726 with the 365-day method — a $24 difference that favors the lender.

Common Mistakes to Avoid

- Forgetting to convert the rate: Using 5 instead of 0.05 in the formula inflates your result by 100x. Always divide the percentage by 100 before multiplying.

- Using months as years: Entering 18 (months) as T instead of 1.5 (years) gives you 12x the correct interest. On a $30,000 loan at 7%, this mistake shows $37,800 instead of $3,150.

- Confusing simple with compound:If your savings account advertises "5.00% APY," that's already a compound rate. Applying I = PRT with that rate underestimates your actual earnings. Use the APY calculator to convert between nominal rates and APY.

- Ignoring fees and origination costs: A $20,000 loan at 5% simple interest sounds like $1,000/year, but a 2% origination fee adds $400 upfront. Your effective cost in year one is $1,400, not $1,000.

Where Simple Interest Is Used in Real Life

Auto loans:Most car loans in the U.S. use simple interest. Your monthly payment covers that month's accrued interest first, and the rest reduces the principal. Paying early — even by a few days — saves money because less daily interest accrues.

Student loans (during grace/deferment):Federal student loans accrue simple interest while you're in school or during grace periods. On a $35,000 loan at 5.5%, that's $5.27 per day in interest piling up before you start repaying.

Promissory notes: Personal loans between individuals typically specify simple interest. A $15,000 note at 4% for 2 years means the borrower pays back $16,200 — straightforward and easy for both parties to verify.

Treasury bills and short-term bonds: T-bills are sold at a discount and pay face value at maturity. The return is calculated using simple interest because the holding period is under one year.

Installment purchases: Some buy-now-pay-later plans and furniture store financing use simple interest rather than compounding, making total costs transparent and predictable.

Tips for Borrowers and Savers

- Make payments early on simple interest loans. Because interest accrues daily on the remaining principal, paying even one week early each month can save hundreds over a 5-year auto loan.

- Compare the total cost, not just the rate. A 4% simple interest loan for 5 years on $20,000 costs $4,000 in interest. A 5% loan for 3 years on the same amount costs $3,000. The higher rate actually costs less because of the shorter term.

- Use simple interest for quick mental math. Need a rough estimate? 5% on $10,000 is $500/year — just multiply the principal by the rate. No compounding tables needed for ballpark figures.

- Watch for hidden compounding.Some lenders advertise "simple interest" but compound unpaid interest into the principal (capitalization). Read the fine print to confirm interest is truly non-compounding.

- For long-term savings, choose compounding.If you're saving for 10+ years, simple interest leaves money on the table. A high-yield savings account with daily compounding earns significantly more than a simple interest instrument over the same period.

When to Use This Calculator

- Evaluating a car loan offer:Plug in the loan amount, dealer's quoted rate, and term to see your total interest cost before signing.

- Drafting a promissory note: Calculate the exact repayment amount for a personal loan between family or friends.

- Estimating T-bill returns: Enter the face value, discount rate, and holding period in days to project your short-term yield.

- Homework and exam prep: Verify I = PRT calculations for finance, accounting, or math coursework with instant results.

- Comparing simple vs. compound interest:Use the built-in comparison to see exactly how much more (or less) you'd earn or pay under each method.